Government mandates for healthcare providers to report quality & improve the performance of care provided, increase in the volume of unstructured data in the healthcare industry, and need to curtail healthcare costs & medical errors are the major factors driving the growth of the market. However, data security concerns and the high cost of quality reporting are expected to restrain the growth of this market to a certain extent.

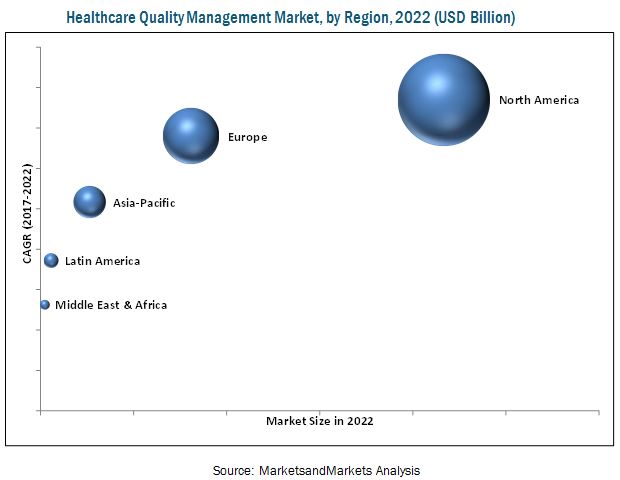

"The global Healthcare Quality Management Market is projected to reach USD 3.31 Billion by 2022 from USD 1.51 Billion in 2016, at a CAGR of 14.2%"

The global market is segmented on the basis of type, delivery mode, application, end user, and region.

This report also provides market information on major regional segments, namely, North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

Download FREE Brochure @ https://www.marketsandmarkets.com/pdfdownload.asp?id=64588778

On the basis of type, the market is segmented into business intelligence & analytics solutions, physician quality reporting solutions, clinical risk management solutions, and provider performance improvement solutions. In 2016, the business intelligence & analytics solutions dominated the market. The large share of this segment can primarily be attributed to the need of healthcare providers to reduce the soaring operating costs, rising demand for quality healthcare, government measures to promote value-based care, and the increasing number of claims denied from insurers.

Based on delivery mode, the web-& cloud-based solutions dominated the market. The large share of this segment is mainly attributed to the flexibility of working from remote areas, affordability, and automated updating features of web-& cloud-based solutions.

By application, the market is classified into data management and risk management. The data management segment is expected to register the highest CAGR during the forecast period. The large share of this segment is attributed to the increasing volume of disparate data and the requirement of quality-based reports by regulatory bodies.

The major end users of healthcare quality management market are hospitals, ambulatory care centers, payers, and ACOs. The hospitals segment accounted for the largest share of the global market in 2016. Growing HCIT adoption, increasing focus on patient safety, significant growth in healthcare spending, rising medical error rates, increasing healthcare costs, and government mandates to follow quality measures are the major factors supporting the adoption of healthcare quality management solutions in hospitals.